A 1,000-GPU cluster costs $30M+. Traditional equipment financing takes 60-90 days to approve. In AI infrastructure, 60 days might as well be a year. By the time the check clears, the customer contracts you were chasing have gone to a competitor who moved faster.

That mismatch between GPU costs and financing speed is why a new category of financing has emerged: operating leases, capital leases, GPU-backed loans, and consumption models, each built for the specific economics of AI hardware.

The Unique Challenge Of GPU Financing

GPUs are not servers. This sounds obvious, but most lenders still treat them the same way.

NVIDIA ships a new architecture every 40 months. H100, then H200, then B200. A single H100 runs $25K-$40K. Deploy a thousand of them and you're looking at $30M in hardware before you've spent a dollar on power, cooling, or real estate. Enterprise data centers routinely face $5M-$100M+ GPU deployments, and paying cash for all of it would gut the operating budget.

Traditional IT equipment lasts 5-7 years and depreciates gradually. GPUs lose 30-50% of their value in 2-3 years because something better is always six months away. Traditional lenders don't price for that kind of depreciation. Their approval timelines assume you can wait. Their rates assume the collateral holds value. Neither assumption works for AI hardware.

Comparing Key Financing Models

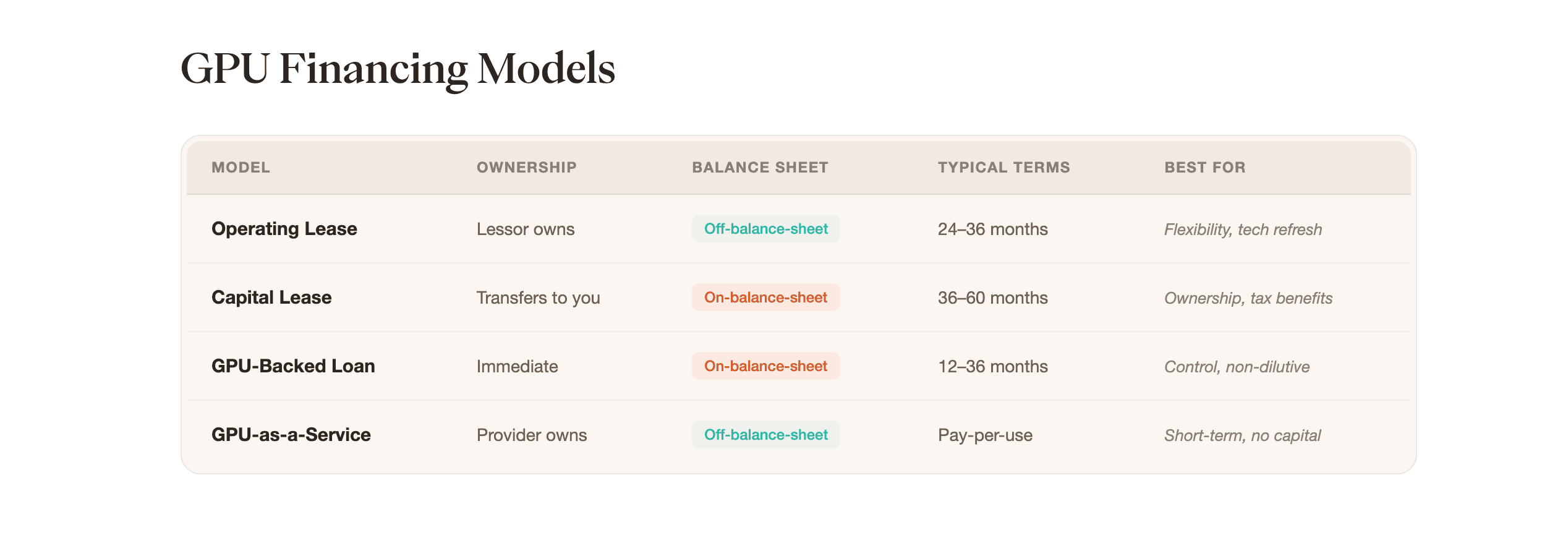

Four models dominate GPU financing today. They differ on three axes: who owns the hardware, how it hits your balance sheet, and who bears the depreciation risk.

1. Operating Leases

Think of this as renting. The financing company owns the GPUs. You pay monthly to use them. When the term ends, you return the equipment, renew, or buy at market value.

The appeal is balance sheet treatment. Lease payments are operating expenses, not debt. Your debt-to-equity ratio stays clean, and you can swap to newer GPUs when the lease expires. Budgeting is simple because the payments are fixed.

The trade-off is ownership. After 36 months of payments, you've built zero equity. Total payments typically exceed the purchase price by 20-40%. Some lessors also restrict how or where you deploy the hardware.

If your priority is balance sheet flexibility and you plan to refresh GPUs every few years anyway, operating leases make sense. If you want to own what you're paying for, keep reading.

2. Capital Leases

A capital lease (also called a finance lease) is a purchase disguised as a lease. The term covers most of the GPU's useful life, and at the end you own the hardware outright, usually for a token $1 buyout.

Unlike operating leases, capital leases sit on your balance sheet as both an asset and a liability. That means they affect your debt ratios. But you also get to claim depreciation for tax purposes, and the total cost runs 15-25% cheaper than an equivalent operating lease because there's no residual value markup.

The risk is straightforward: you own the asset, so you own the depreciation. If those H100s are worth half what you paid in three years, that's your problem. You're also locked into specific hardware for the full term.

This works for operators with strong balance sheets who are comfortable with depreciation exposure and want the tax benefits of ownership.

3. GPU-Backed Loans

This is the most direct option. You borrow money. The GPUs are your collateral. The lender takes a security interest in the hardware, and if you default, they seize and sell it.

Typical LTV ratios range from 50% to 80% of the GPU purchase price. You repay over 12-36 months, principal plus interest. The GPUs stay in your data center running your workloads the entire time. Loans come in two flavors: non-recourse (the lender can only take the collateral) and recourse (they can come after your other assets too).

This is the cheapest form of financing because there's no lessor margin baked in. You own the GPUs from day one. You control where they go and what they run. The catch: you need 20-50% down, and traditional lenders take 45-90 days to underwrite. Blockchain-enabled lenders like GPULoans.com have compressed that to 7 days by using tokenized collateral and on-chain verification, but the down payment requirement remains.

4. GPU-As-A-Service

Pay per GPU-hour. The provider owns, maintains, and upgrades the hardware. You just consume compute. Rates typically run $2-$5/hour for H100 equivalent capacity.

No capital outlay. Instant scaling. Zero depreciation exposure. Sounds perfect until you look at the math over time. At 24+ months, GPUaaS costs 3-5x what owned hardware would run you. A 500-GPU deployment at $3/hour for 36 months is $47M. The same hardware purchased outright is $15M.

GPUaaS is the right answer for short-term projects, proof-of-concept work, or when you need capacity tomorrow and can't wait for any financing approval. It is the wrong answer for steady-state production workloads.

Advanced Approaches For Data Centers

The four models above cover most situations. Larger operators with more complex balance sheets sometimes use hybrid structures.

1. Sale-Leaseback Arrangements

You sell GPUs you already own to a financing company for cash, then immediately lease them back. The hardware never moves. You keep running your workloads. The financing company takes ownership and you start making lease payments.

You'll typically get 60-80% of current market value in cash. The 20-40% haircut is the financing company's margin for taking on the depreciation risk.

Sale-leasebacks are useful when you need liquidity for expansion but don't want to disrupt running infrastructure, or when you want to move owned assets off your balance sheet. The downside is that you're now paying rent on equipment you used to own free and clear.

2. Tokenized Collateral Structures

This is where GPU financing meets DeFi, and it's where the biggest efficiency gains are happening.

The setup: a bankruptcy-remote SPV takes legal ownership of the GPUs. A third-party data center issues a UCC Article 7 Electronic Warehouse Receipt confirming custody. That receipt gets tokenized on-chain (typically ERC-20 on Ethereum or Arbitrum) and deposited into a smart contract. The lender advances up to 80% LTV against the tokenized collateral.

What makes this different from a traditional equipment loan is speed and transparency. Lenders verify GPU location, specs, and status on-chain in real time. There's no 60-day underwriting process because the collateral is continuously verifiable. DeFi capital markets eliminate the overhead of traditional banking, cutting rates 20-30% compared to conventional equipment loans.

The non-recourse SPV structure also means your liability is limited to the pledged hardware. If GPU prices collapse, the lender takes the collateral and that's it. Your other assets are protected.

The complexity is real. SPV formation, legal docs, and blockchain integration make this uneconomical below $1M. Some finance teams also need education on how tokenized collateral works. But for deals above that threshold, the speed and cost advantages are substantial.

3. Synthetic Lease Setup

A synthetic lease gives you the best of both worlds on paper: off-balance-sheet treatment for accounting, but tax ownership (meaning you claim depreciation). Terms are typically 3-5 years with a purchase option at a predetermined price.

Getting this dual treatment right requires careful structuring. You need it to qualify as an operating lease under ASC 842 and IFRS 16 while simultaneously meeting ownership criteria for tax purposes. If GPUs depreciate faster than expected, your purchase option might end up above market value, which creates an awkward decision at the end of the term.

Off-Balance-Sheet And Tokenized Options

Why do data centers care so much about keeping assets off the balance sheet?

Three reasons. First, many have loan covenants with banks that cap their debt-to-equity ratios. Off-balance-sheet financing doesn't count against those limits. Second, Moody's and S&P factor debt levels into credit ratings. Third, venture-backed operators want to show capital efficiency: low asset intensity, high returns on invested capital.

Operating leases, sale-leasebacks, and GPUaaS all stay off the balance sheet. Capital leases and GPU-backed loans go on it. Tokenized structures can go either way depending on SPV setup.

The real differentiator with tokenized approaches isn't the balance sheet treatment. It's the 7-day approvals and 20-30% lower rates. When you're trying to close a $50M GPU deployment before a competitor does, the difference between a week and three months matters more than where it sits on your financials.

Evaluating Cash Flow And Risk

1. Depreciation And Resale Values

NVIDIA's 18-24 month release cycle means an H100 purchased for $30K in 2023 might be worth $15K-$20K by 2026 when B200 and B300 are shipping.

Who bears that risk depends entirely on your financing model. Operating leases and sale-leasebacks push it to the lessor. Capital leases and GPU-backed loans leave it with you. GPUaaS pushes it to the provider.

If you think sustained AI demand will hold resale values, ownership models save you money. If you think the next architecture will crater current GPU prices, lease it.

2. Utilization And Scalability Risk

Financed GPUs that sit idle still cost money. At 80%+ utilization, ownership models are cheapest. At 30-70% utilization, operating leases give you room to adjust. If utilization is genuinely unpredictable, GPUaaS is the only model where your costs track your actual usage.

3. Default And Collateral Implications

What happens when payments stop?

Operating leases and sale-leasebacks: the lessor takes the GPUs back. You lose capacity immediately and may owe early termination fees. Capital leases: same outcome, since the lessor holds security interest until the last payment.

GPU-backed loans depend on recourse terms. Non-recourse means the lender takes the collateral and walks away. Your other assets are untouched, especially if you structured through a bankruptcy-remote SPV. Recourse means the lender can pursue your other assets beyond the hardware.

GPUaaS: the provider turns off access. No collateral implications because you never owned anything.

Decision Framework For Enterprise Data Centers

1. Assessing Financial Health

Start with your balance sheet. Debt-to-equity below 1.5, 12+ months of runway, and positive EBITDA (or a clear path to it) means you have access to ownership models: capital leases and GPU-backed loans. These are cheaper over time and build equity.

Debt-to-equity above 2.0, less than 6 months runway, or uncertain revenue means you're better off with operating leases, sale-leasebacks, or GPUaaS. Keep assets off the balance sheet and preserve cash.

2. Building A Comparative Cost Matrix

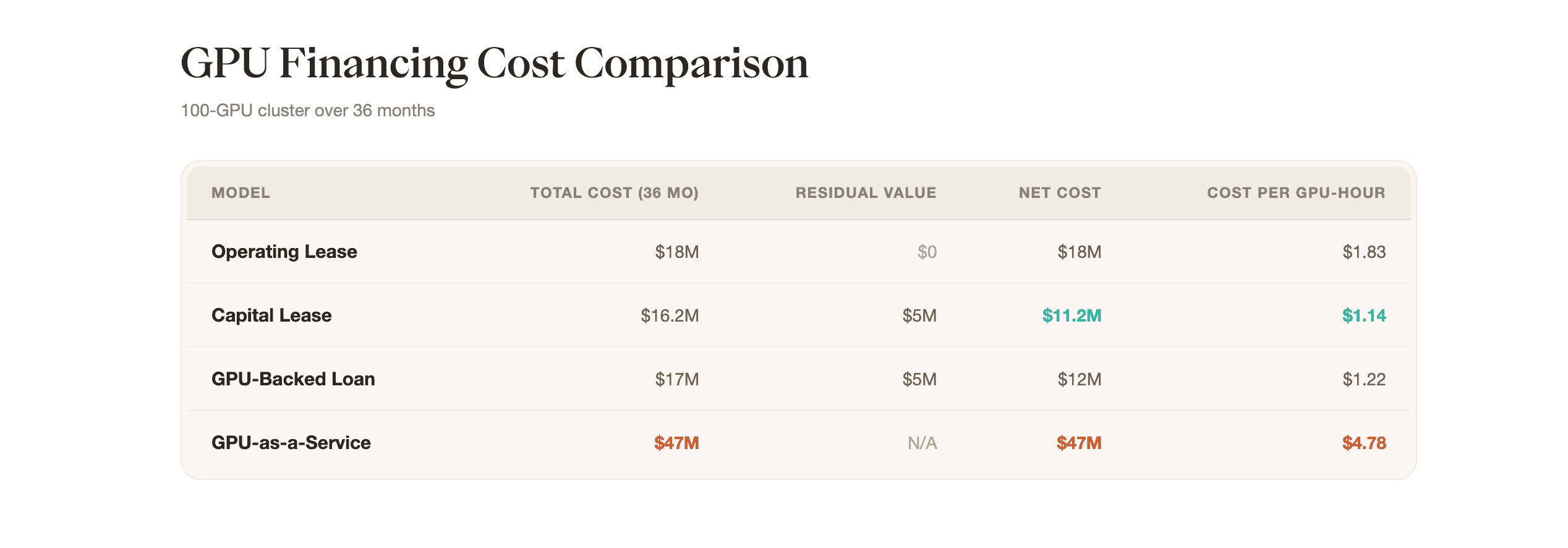

Calculate total cost of ownership (TCO) across models. First, define your scenario: GPU type and quantity (500 H100s at $30K each = $15M hardware cost), deployment timeline (36 months), and expected utilization rate (75%).

Second, calculate costs for each model. Operating leases might run $500K/month × 36 months = $18M total. Capital leases might run $450K/month × 36 months = $16.2M total. GPU-backed loans might be $15M hardware + $2M interest = $17M total. GPU-as-a-Service might be $3/hour × 24 hours × 365 days × 36 months × 500 GPUs = $47M total.

Third, factor in depreciation and resale for ownership models. If H100s are worth $10K each after 36 months, 500 GPUs = $5M residual value. That makes the adjusted TCO for a GPU-backed loan $17M - $5M = $12M net cost. Fourth, compare TCO per GPU-hour by dividing total cost by (GPUs × hours × utilization). For example, $12M ÷ (500 × 26,280 hours × 75%) = $1.22/GPU-hour.

The difference between the cheapest model (capital lease at $1.14/GPU-hour) and GPUaaS ($4.78/GPU-hour) is 4x. At scale, that's the difference between a profitable AI operation and one that's subsidizing its compute provider.

3. Aligning With Long-Term AI Strategy

Planning to double capacity in 12 months? Operating leases or GPUaaS let you scale without re-underwriting every purchase. Running stable, predictable workloads? Ownership models lock in the lowest long-term cost. Need the newest hardware at all times? Leases with upgrade provisions keep you current.

What's Changing In GPU Financing

Three trends are reshaping this market.

Traditional banks are building GPU-specific lending desks. Private credit funds (Blackstone, Apollo, Magnetar) are raising vehicles dedicated to AI infrastructure. Blockchain-enabled lenders are using DeFi capital markets to offer faster, cheaper financing with real-time collateral tracking.

On the collateral side, lenders are adopting tokenized warehouse receipts (UCC Article 7), IoT monitoring of GPU location and temperature, and smart contract-based liquidation triggers. As lender confidence in GPU resale markets grows, LTV ratios are climbing from 50-60% to 70-80%, terms are stretching from 24 months to 36-48, and non-recourse structures are becoming the default.

NVIDIA and data center operators like CoreWeave and Lambda are also starting to bundle financing directly at the point of purchase. Single contracts covering hardware and capital. The friction between "I need GPUs" and "I have GPUs" continues to shrink.

Finance Your Next GPU Deployment

Four models, each with clear trade-offs. Operating leases for flexibility. Capital leases for cost-efficient ownership. GPU-backed loans for control and speed. GPUaaS for variable, short-term needs. Advanced structures like sale-leasebacks, tokenized collateral, and synthetic leases add more options for larger operators.

Which one fits depends on your balance sheet, your utilization patterns, and how fast you need to move. Traditional equipment financing takes months. Tokenized collateral structures close in a week and cost 20-30% less.

If you're deploying $1M+ in GPU infrastructure, GPULoans.com offers non-recourse, asset-backed financing with 7-day approvals and up to 80% LTV. Terms built for AI hardware economics, not legacy equipment assumptions.

FAQs About GPU Financing For Data Centers

What is the typical approval timeline for GPU-backed loans?

Traditional equipment lenders take 60-90 days. Blockchain-enabled lenders using tokenized collateral close in 7-30 days.

Can data centers finance GPUs that are already deployed?

Yes. Sale-leaseback arrangements let you sell deployed GPUs to a financing company for 60-80% of market value and immediately lease them back. The hardware stays in your data center.

What LTV can I expect for NVIDIA H100 financing?

50-70% with traditional lenders. Up to 80% with specialized GPU lenders who understand AI hardware depreciation and resale markets.

Do GPU financing payments qualify as operating expenses?

Operating lease payments do. Capital leases and GPU-backed loans create depreciable assets on your balance sheet. Talk to your tax advisor for specifics.

What if my AI workload demand drops after financing?

Operating leases let you return or scale down at term end. Under ownership models, you bear the risk of idle hardware but can redeploy the GPUs or sell them on the secondary market.

Can I finance GPUs from multiple vendors in one deal?

Most lenders will cover mixed deployments (NVIDIA H100/H200/B200, AMD MI300) within a single facility. LTV ratios may differ by model based on each GPU's resale liquidity.

How does tokenized GPU collateral differ from a traditional equipment lien?

Traditional liens use paper-based UCC-1 filings and take 60-90 days to process. Tokenized structures use blockchain-based Electronic Warehouse Receipts (UCC Article 7) with real-time verification and programmable liquidation, closing in 7 days.

What credit score or financials do I need to qualify?

It depends on the model. Operating leases look at cash flow and revenue stability. GPU-backed loans prioritize collateral value and may work for startups with strong customer contracts. GPUaaS usually has no credit requirements at all.