GPU financing typically costs between 10% and 17% APY—a rate that sits noticeably above traditional bank loans but reflects the deep structural risks that regulated banks are increasingly unable to take on. This pricing, often expressed as a floating rate (e.g., SOFR + 500-700 basis points), is set by Private Credit funds. The rate reflects how these specialized lenders view the unique risks of GPU collateral: rapid technological obsolescence, volatile resale markets, and the capital-intensive regulatory environment (Basel III) that displaces traditional banks from this market.

This article breaks down why GPU loans carry these rates, compares them using specific examples of recent financing deals, and explains how this cost of capital is fundamentally reshaping AI infrastructure investment.

What is GPU cost of capital?

A typical yield for specialized GPU financing currently sits in the 10% to 17% range, defined by private credit's target return hurdle, rather than traditional banking spreads. This range is significantly higher than traditional bank loans (typically 5% to 10% for strong corporate borrowers) but slightly below the rates seen in emerging, unproven Decentralized Finance (DeFi) platforms (which can reach 13-17% APY). This higher rate reflects the specialized nature of GPU assets, which carry risks like rapid technological obsolescence and market volatility that regulated banks struggle to evaluate, particularly under the punitive risk-weighting standards of Basel III.

Cost of capital refers to the minimum return required to justify an investment. For GPU-intensive businesses, this calculation is highly complex because the hardware depreciates faster than most business assets while generating highly volatile, short-term revenue through compute services. The weighted average cost of capital (WACC) blends both debt and equity costs into a single metric that shows your true financing expense.

GPUs occupy an unusual position in the lending world. Unlike real estate or manufacturing equipment, these assets can lose 30-50% of their value within 12-18 months as new chip architectures emerge. Lenders price this technological risk directly into their rates. Traditional banks are further constrained by regulatory rules, such as the Basel III Supervisory Slotting Approach, which can assign a prohibitive 115% or 250% Risk Weight (RW) to Object Finance (like GPU leasing), making it mathematically impossible for them to compete with private credit on price.

Why 12–15% APR is common for GPU financing (Private Credit View)

The typical 12% to 15% yield range is primarily the target return hurdle for large private credit funds like Blackstone or Magnetar. This yield covers their cost of funds, internal operational costs, and the equity risk premium required by their investors.

This rate reflects three interconnected risk factors that private credit is structured to accept, unlike traditional banks.

1. Depreciation and Collateral Risk

Lenders justify their yield by factoring in a "B200 Cliff" risk, where a new chip (like Nvidia’s Blackwell) causes the value of current collateral (like H100s) to drop suddenly. To protect against this, specialized lenders structure loans with short amortization schedules, such as Crusoe Energy’s 3.5-year repayment term for its 20,000 GPU facility, ensuring the loan is paid down faster than the asset’s economic life.

2. Market Volatility and Concentration

GPU prices are highly volatile. This is compounded by Concentration Risk. For example, CoreWeave’s credit profile is heavily reliant on its multi-billion dollar contracts with anchor tenants like Microsoft and OpenAI. A lender's exposure is not just to the hardware, but to the continued demand from a very small number of customers.

3. Structural and Regulatory Dislocation

The reason private credit dominates this space is regulatory arbitrage. While a bank lending to an unrated GPU Special Purpose Vehicle (SPV) may face a 100% Risk Weight under Basel III (forcing them to hold $10.5 million of capital for every $100 million lent), a private credit fund faces 0% regulatory capital charges. The bank must charge an exorbitantly higher rate just to cover its regulatory capital cost, while private credit only needs to cover its funding cost (the LP hurdle rate). This structural inefficiency makes the bank uncompetitive.

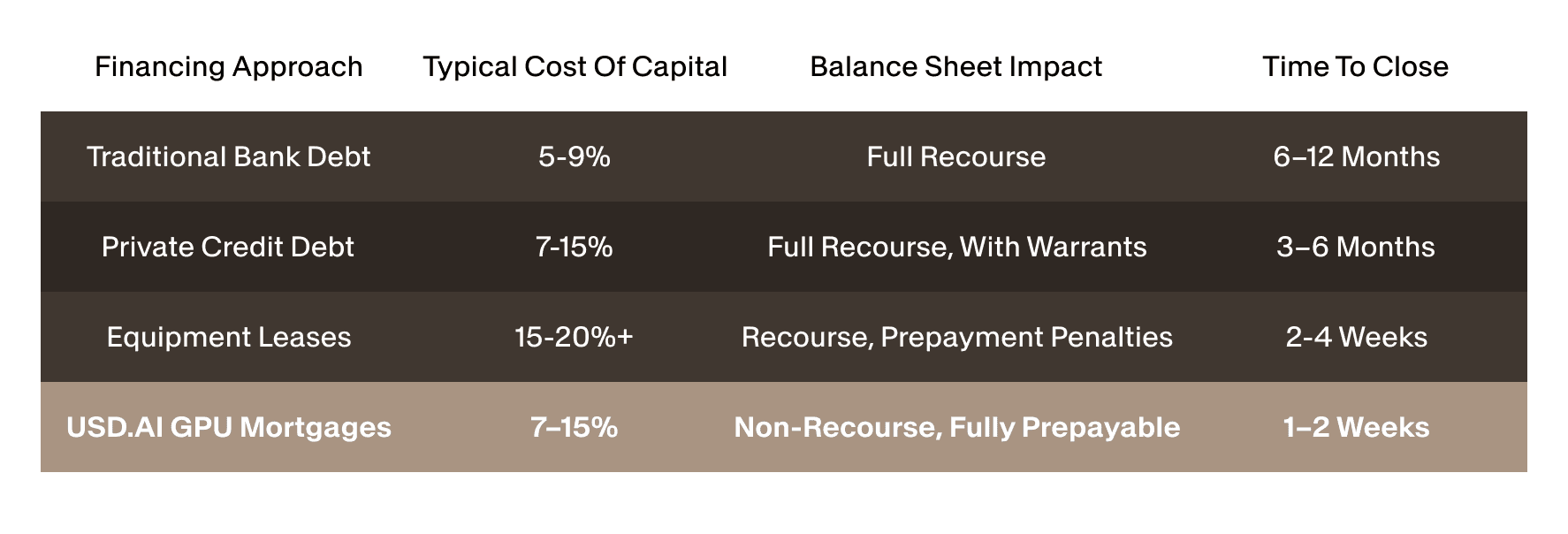

Comparing Traditional Credit to GPU-Focused Loans

The differences extend beyond the interest rate. The type of collateral and the speed of execution are critical.

Weighted average cost of capital example for GPU SPVs

The weighted average cost of capital (WACC) calculation becomes particularly important for GPU deployments because most operators use a mix of debt and equity financing. Understanding your true cost of capital helps you make better decisions about deployment scale and customer pricing.

1. Calculating cost of debt

To find your after-tax cost of debt, multiply your interest rate by one minus your tax rate. Interest expenses reduce your taxable income, creating a tax shield that effectively lowers your borrowing cost. For example, a 14% APR with a 25% tax rate results in a 10.5% after-tax cost of debt (14% × 0.75 = 10.5%).

This tax benefit makes debt financing more attractive than the headline rate suggests, particularly for profitable operations with significant tax liability.

2. Estimating cost of equity

Equity investors in GPU ventures typically require returns of 20-30% to compensate for the technology risk and operational complexity. This expected return reflects not just the financial risk but also the opportunity cost of investing in GPU infrastructure versus other technology ventures.

You can estimate your cost of equity using the Capital Asset Pricing Model (CAPM), which adds a risk premium to the risk-free rate based on your business's volatility relative to the broader market. However, many GPU operators simply use the return expectations that equity investors explicitly state during fundraising.

3. Finding the capital mix

Weight your debt and equity components based on their proportion of total financing. A typical GPU SPV might use 60% debt and 40% equity, though this ratio varies based on the operator's risk tolerance and available financing options.

For a GPU deployment with 60% debt financing at 14% APR (10.5% after tax) and 40% equity financing at 25% required return, the WACC calculation would be: (10.5% × 0.6) + (25% × 0.4) = 16.3%. This means every dollar invested in GPUs needs to generate at least 16.3% annual return to meet your financing obligations and investor expectations.

How to lower rates and improve terms on GPU loans

While 12-15% APR represents the typical market rate for GPU financing, several approaches can help you secure terms at the lower end of this range or even below it.

1. Strengthening revenue contracts

Secured customer contracts reduce lender risk by providing visibility into your revenue stream. A three-year contract with a creditworthy customer for GPU compute services gives lenders confidence that you'll generate the cash flow needed to service debt, even if the hardware value declines.

Some lenders will reduce rates by 100-200 basis points if you can demonstrate contracted revenue covering 80% or more of your debt service obligations. The contract quality matters too—agreements with established enterprises carry more weight than those with early-stage startups.

2. Enhancing collateral quality

The condition and documentation of your GPU assets directly impacts lending terms. Maintaining detailed usage logs, temperature monitoring data, and maintenance records demonstrates operational discipline that lenders value. Newer GPU models with longer expected useful lives also command better financing terms than hardware approaching end-of-life.

Operating in Tier 3 or Tier 4 data centers with robust power and cooling infrastructure reduces lender concerns about environmental damage to the hardware.

3. Negotiating with specialized lenders

GPU-focused lenders compete for quality borrowers, particularly operators with strong track records and growth potential. If you've successfully completed previous financings and maintained good payment history, you have leverage to negotiate better terms on subsequent loans.

Building relationships with multiple lenders creates competitive tension that works in your favor. When lenders know you have alternatives, they're more likely to sharpen their pencils on rate and terms.

Building a sustainable GPU financing strategy

A long-term approach to GPU financing balances cost of capital against operational flexibility. As your deployment scales from dozens to hundreds or thousands of GPUs, your financing strategy evolves to match your operational maturity.

Early-stage operators often accept higher rates in exchange for speed and flexibility, prioritizing rapid deployment over minimizing financing costs. As you build operational history and customer relationships, you can gradually shift toward lower-cost financing options that reward your track record. This progression might mean starting with 15% APR non-recourse loans and moving toward 10-12% rates as you demonstrate consistent performance.

Finance your next GPU deployment with partners who understand AI infrastructure and can structure financing that aligns with your hardware refresh cycles and revenue patterns.

Hardware lifecycle management plays a crucial role in financing strategy. Aligning your loan terms with expected GPU useful life prevents situations where you're still paying for obsolete hardware. Most operators target loan terms of 24-36 months for high-end GPUs, matching the period when the hardware remains competitive for demanding workloads.

FAQs about GPU financing

What happens if my GPUs become obsolete during the loan term?

Most GPU financing agreements include provisions for hardware refreshes or upgrades that protect both lender and borrower from technological obsolescence risk. You can typically refinance or restructure the loan to swap out older hardware for newer models, though this may involve paying down a portion of the existing loan or accepting adjusted terms based on the new collateral's value.

How quickly can I access funds through a GPU-backed loan?

Specialized GPU lenders typically process applications in 7-30 days, significantly faster than traditional bank loans which often require 30-90 days for approval and funding. The exact timeline depends on factors like the complexity of your SPV structure, the number of GPU units being financed, and how quickly you can provide required documentation and insurance.

What determines whether I qualify for the lower end of the 12-15% APR range?

Your qualification for lower rates depends primarily on your operational track record, the quality and age of your GPU assets, and the strength of your revenue contracts. Operators with established customer relationships, newer hardware, and proven operational discipline typically secure rates closer to 12%, while newer entrants or those with older equipment may see rates toward 15%.

How does weighted average cost of capital calculation differ for GPU-intensive businesses?

GPU-intensive businesses typically have higher WACC calculations due to the technology risk premium applied to both debt and equity components compared to traditional businesses. The rapid depreciation of GPU assets and market volatility increase both debt costs (through higher interest rates) and equity costs (through higher required returns), resulting in WACC figures often 5-10 percentage points above comparable non-technology businesses.

Can I refinance my GPU loans if market interest rates decrease?

Refinancing options exist but often include prepayment penalties in the first 12-24 months. After this period, borrowers with strong payment history can typically refinance at improved rates, particularly if they've grown their revenue base or upgraded their GPU collateral.